News

Rural Banks Can Help Fill The Digital Gap

Southeast Asia, a region with a population of 600 million and projected 2025 GDP of around $4.7 trillion, is one of the fastest growing regions globally.

Despite this growth, the majority of its population is still hesitant to adopt digital transactions. In 2019, 70% of small and medium-sized enterprises (SMEs) preferred cash payments, and 70% of the population was considered “unbanked and underserved.” Until now, SMEs and individuals are still trying to adapt to improved and digitized fintech services like online banking, e-wallets, and credit cards.

Rural banks, which are abundant in Southeast Asia and serve as traditional banks for communities far from urban cities, are uniquely positioned to help bridge this gap. These banks have extensive networks and are experienced in serving the “unbanked and underserved” population, which allows them to establish a trusted relationship with these communities.

With their deep understanding of the needs, preferences, and challenges of the rural sector, they can strategically position fintech companies as a trusted entity that can help these communities.

Bangko Sentral ng Pilipinas (BSP) Assistant Governor Arifa A. Ala believes that rural banks, being the bridge connecting remote areas with the unbanked and underserved and fintech companies, can play a crucial role in encouraging people to transition from traditional transactions to digitized operations.

The regulators can also help curate policies promoting financial inclusion for a wider population, as well as standards and regulations that will help rural banks expedite the process of converting SMEs and rural citizens to digital transactions.

To help alleviate the digital gap in Southeast Asia, there are programs that have been launched in the region:

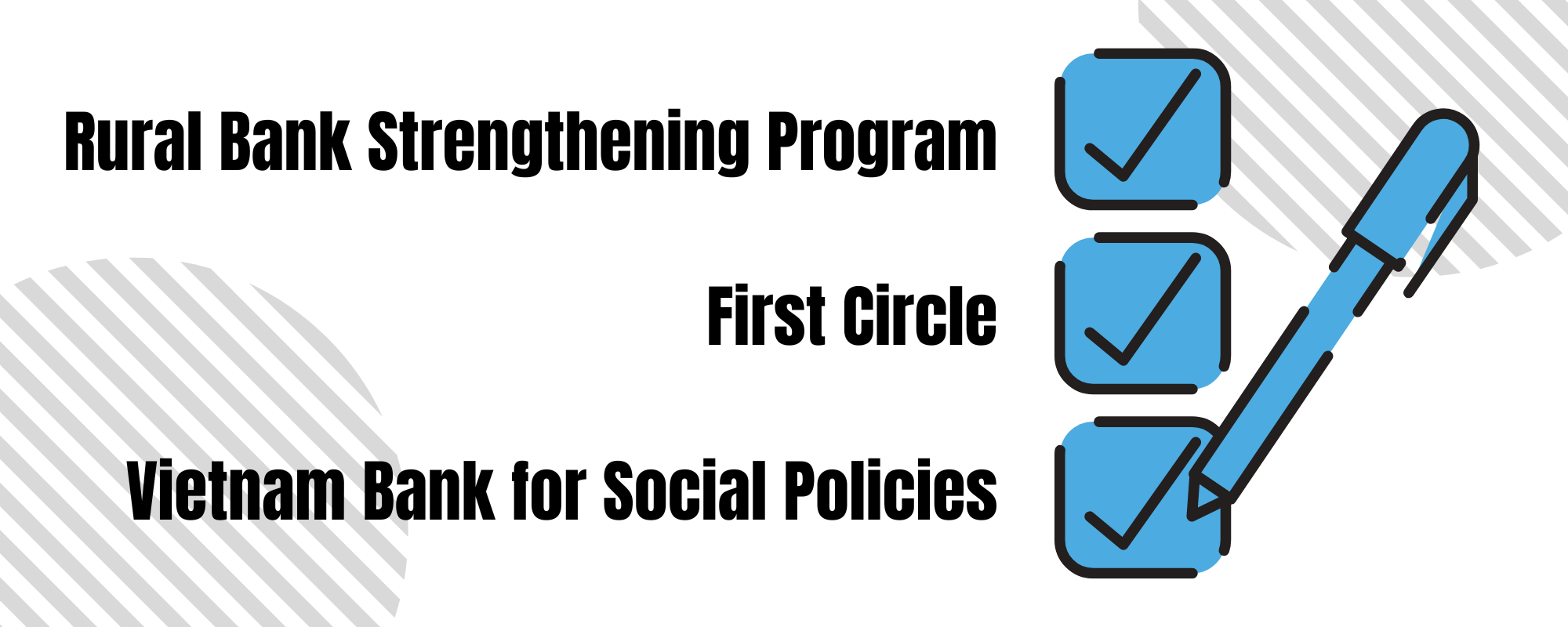

1. Rural Bank Strengthening Program (RSBP) launched in 2022, focuses on:

- Improving the base level of funding

- Promoting incentives to boost digitalization

- Providing sufficient capital for the continuity of rural banks’ operations

- Revising existing regulations that need updates

2. First Circle

- Offers financial services and assistance to SMEs

- Helps raise communities by providing strategic financial solutions

3. Vietnam Bank for Social Policies, established in 2002

- Offers financial solutions at accessible and affordable rates

The role of rural banks in this process cannot be overemphasized as they have the experience, networks, and understanding to help bring the rural communities into the digital economy.